No. 13 - Matheus Grasselli

January 23, 2021Brazilian-Canadian. Professor of Financial Mathematics and Chair of the Mathematics of Statistics Department at McMaster University. He was the Deputy Director of the Fields Institute for Research in Mathematical Sciences in Toronto (2012-2016) and the Director of the Fields Centre for Financial Industries (2017-2020) and is currently a co-leader of the Fields-CQAM lab on Systemic Risk Analytics. He holds a PhD in Mathematical Physics from King’s College London, and has published research papers on information geometry, statistical physics, and several aspects of quantitative finance, including interest rate theory, optimal portfolio, real options, executive compensation, and macroeconomics. He is also the author of an undergraduate textbook on numerical methods. He is a regular speaker in both academic and industrial conferences around the world and has consulted for CIBC, Petrobras, EDF, and Bovespa. He is on the editorial board of numerous journals, including the Journal of Banking and Finance, the International Journal of Theoretical and Applied Finance, and the Journal of Dynamics and Games, and is also the founding managing editor of the book series Springer Briefs on Quantitative Finance. In 2019 he published his first novel, The Venetian Files: the secret of financial crises. Find Matheus newest book at http://www.mosaic-press.com/product/the-venetian-files/

More from the Blog

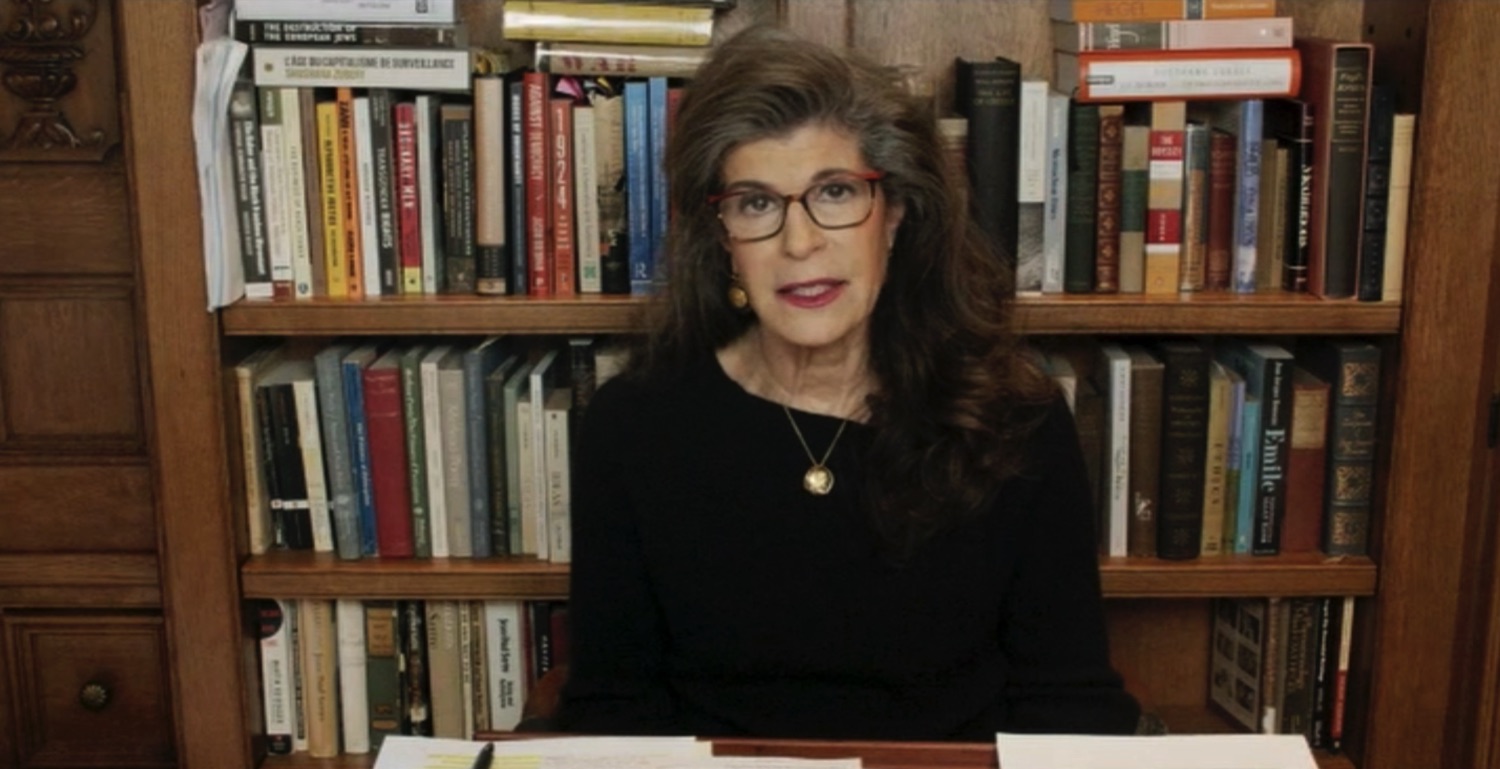

No. 53 - Shoshana Zuboff

Shoshana Zuboff - Trailer

No. 52 - Grigory Yavlinsky

Grigory Yavlinsky- Trailer

No. 51 - Paola Subacchi

Paola Subacchi - Trailer

No. 50 - Barry C. Lynn

Barry C. Lynn - Trailer

No. 49 - Barry Eichengreen

Barry Eichengreen - Trailer

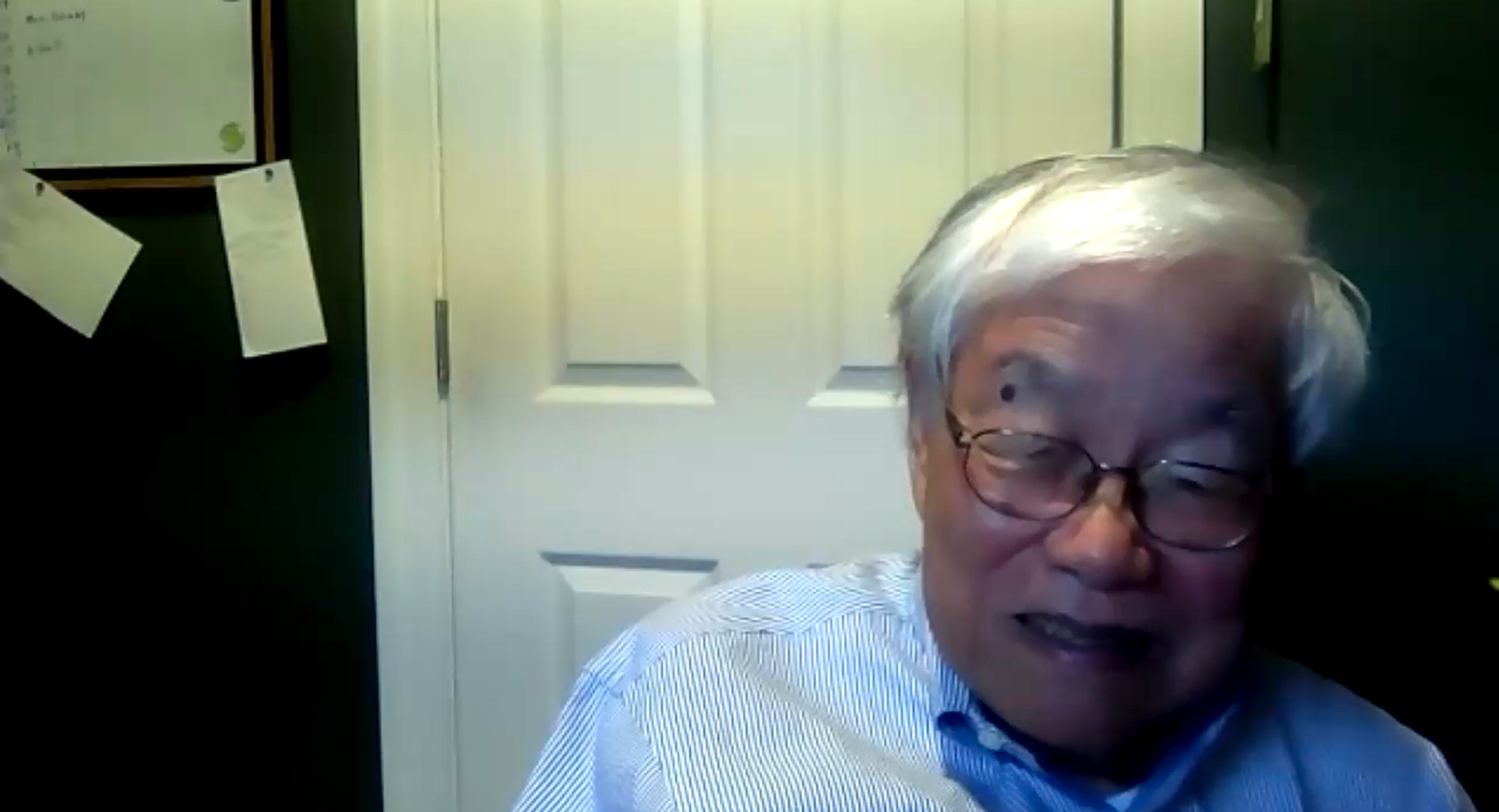

No. 48 - Koichi Hamada

Koichi Hamada - Trailer

No. 44 - Shanaya D’sa/ Leora Schertzer

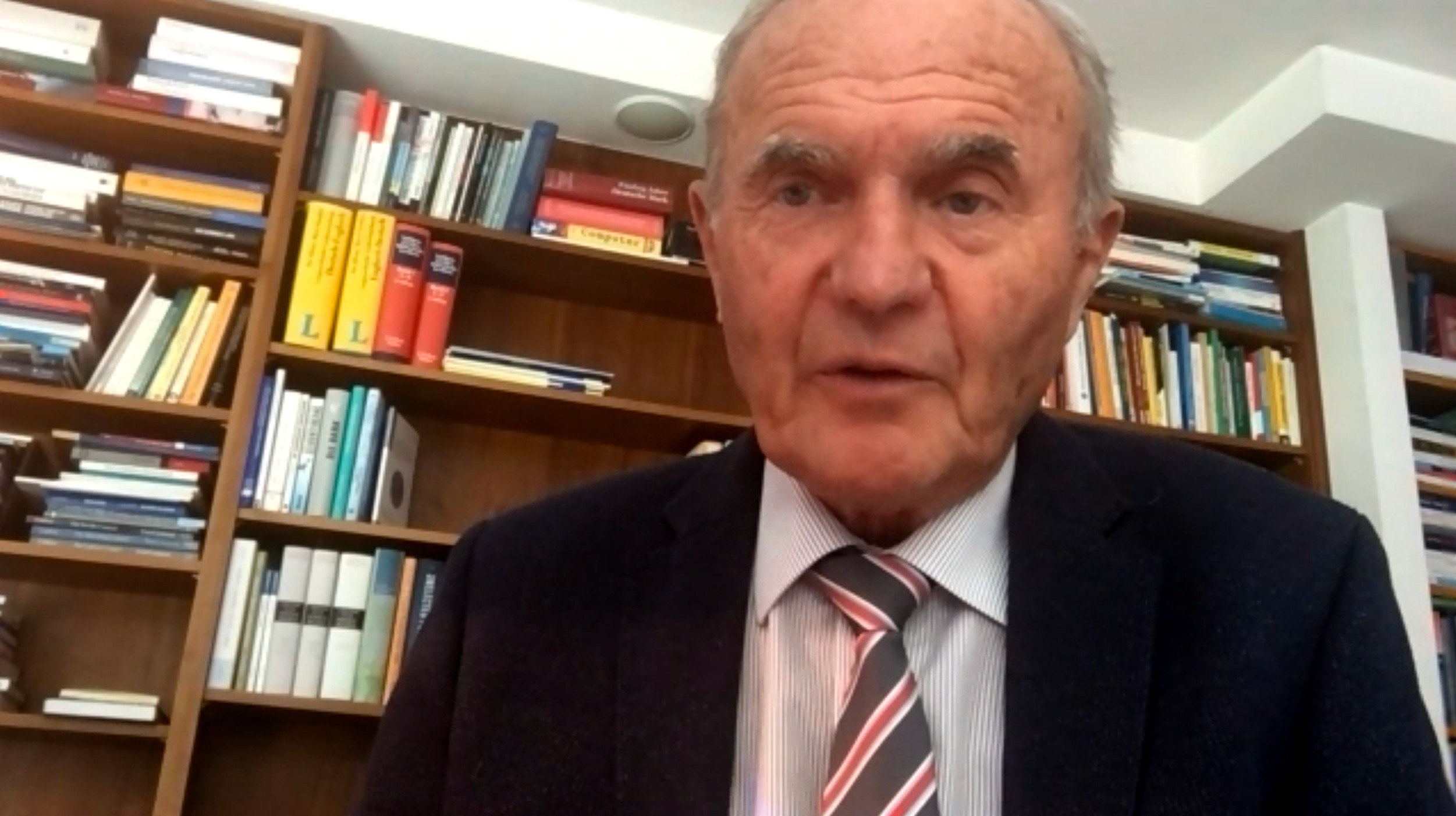

No. 43 - Otmar Issing

Otmar Issing - Trailer

No. 42 - Harris Eyre

No. 41 - Harold James

Harold James - Trailer

No. 40 - Katharina Pistor

No. 39 - Branko Milanović

No. 38 - Ian Hughes

Ian Hughes - Trailer

No. 37 - Laura Pautassi

Laura Pautassi - Trailer

No. 36 - Arunma Oteh

Arunma Oteh - Trailer

No. 35 - Arjun Jayadev and J.W. Mason

No. 34 - Tito Boeri

No. 32 - Anat Ruth Admati

No. 30 - Muhamad Chatib Basri

Sheila Lawlor - Trailer

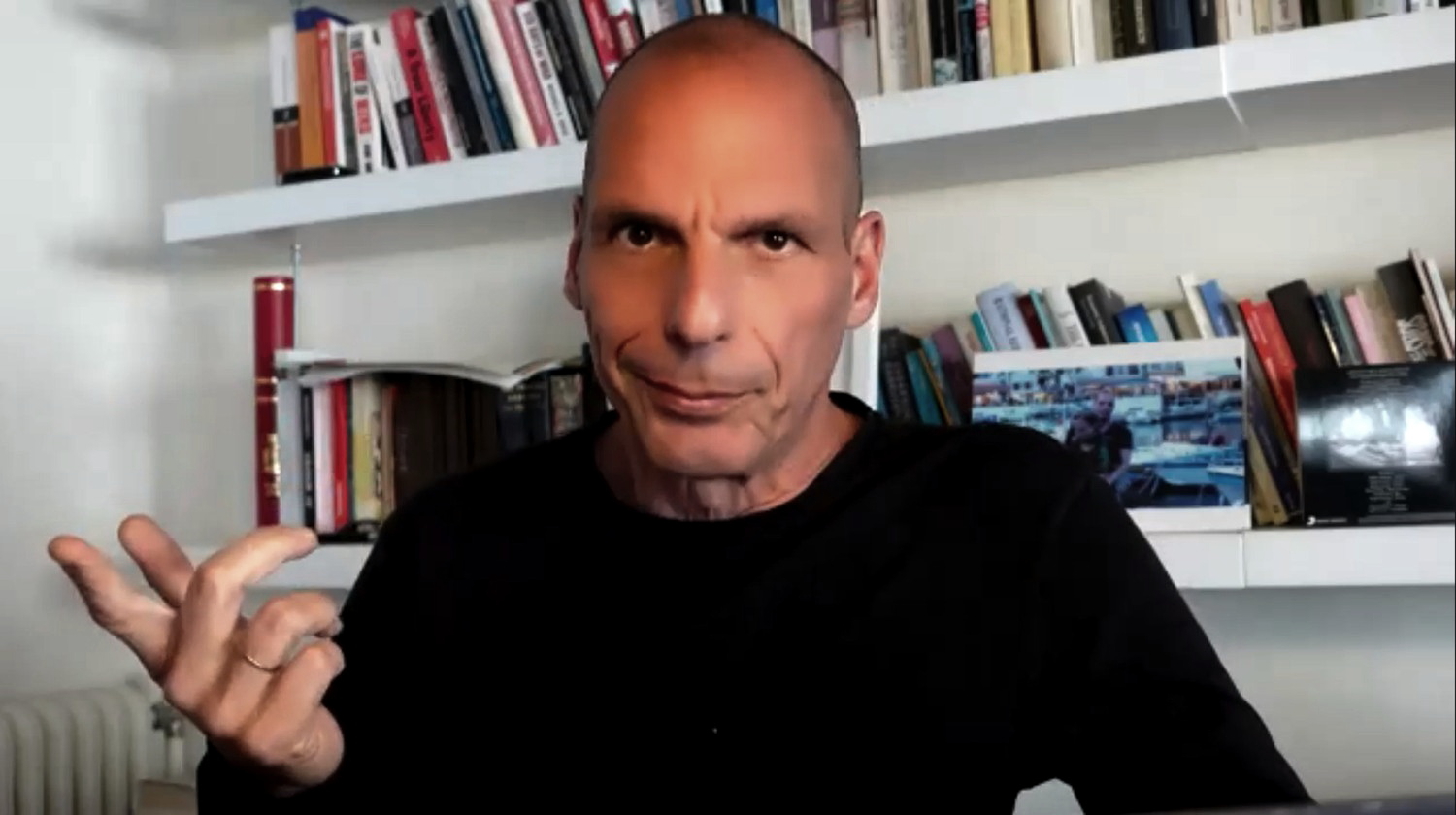

No. 28 - Yanis Varoufakis

Yanis Varoufakis - Trailers

No. 27 - Fred Oleyele

Fred Olayele - Trailer

No. 26 - Rebecca Henderson

Rebecca Henderson - Trailer

No. 25 - Rym Ayadi

Rym Ayadi - Trailer

No. 24 - Thitinan Pongsudhirak

Thitinan Pongsudhirak - Trailer

No. 23 - Hannah Ryder

Hannah Ryder - Trailer

No. 22 - Ann Pettifor

Ann Pettifor - Trailer

No. 21 - Ricardo Hausmann

Ricardo Hausmann - Trailer

No. 20 - Jayati Ghosh

Jayati Ghosh - Trailer

No. 19 - Richard Bookstaber

Richard Bookstaber - Trailer

No. 18 - James K. Galbraith

James K. Galbraith - Trailer

Roundtable #01

No. 17 - HRH Muhammad Sanusi II

HRH Muhammad Sanusi II - Trailer

No. 16 - Mark Blyth

Mark Blyth - Trailer

No. 15 - Albena Azmanova

Albena Azmanova - Trailer

- Why does economics matter? - First trailer

No. 14 - Keyu Jin

Keyu Jin - Trailers

No. 13 - Matheus Grasselli

No. 12 - Carolina Cristina Alves

No. 11 - Jason DeSena Trennert

Jason DeSena Trennert - Trailer

No. 10 - Andrew S. Nevin

No. 9 - Leo Johnson

No. 8 - Penny Mealy

Penny Mealy - Trailer

- What are the differences between economic science and economic engineering? - First trailer

No. 7 - Steve Keen

Steve Keen - Trailer

No. 6 - Noam Chomsky

No. 5 - Roberto Mangabeira Unger

No. 4 - Ludger Schuknecht

No. 3 - Alan Kirman

No. 2 - Rana Foroohar

Rana Foroohar - Trailers

No. 1 - William Hynes